Introduction to Corporate Finance

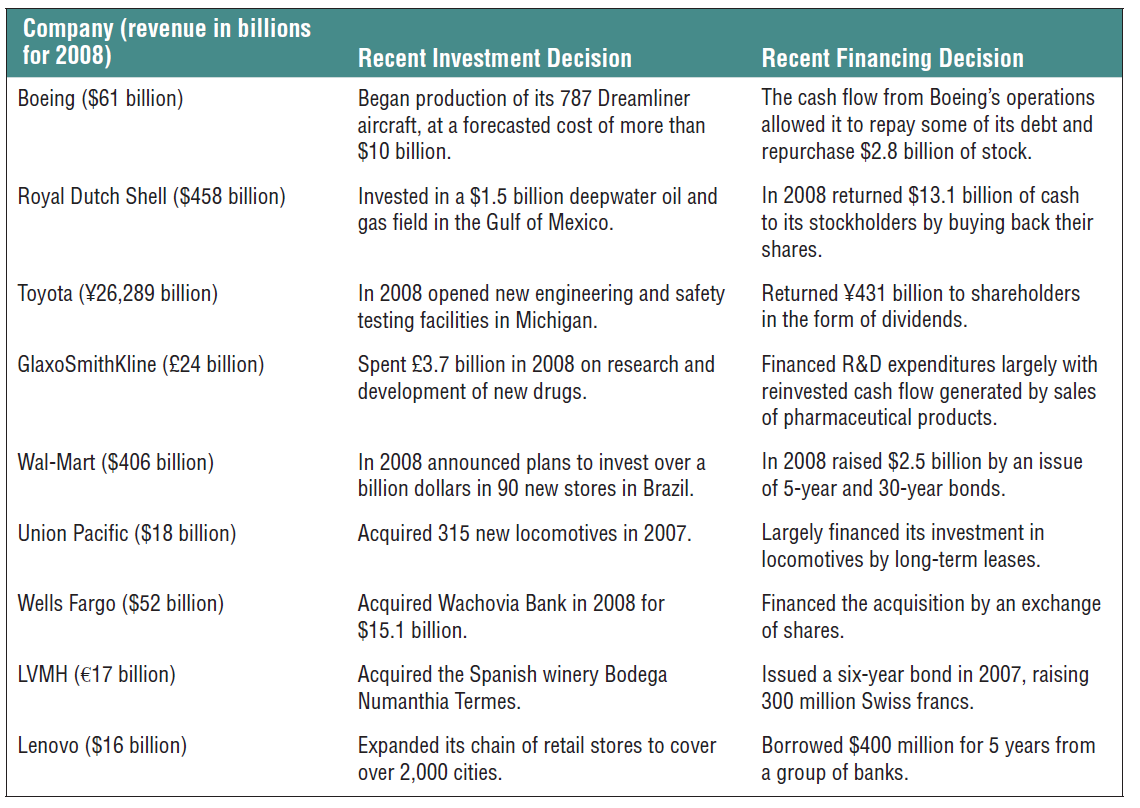

Examples of Investment and Financing Decisions

Managing investment and financing decisions

We saw that any business opportunity must be accompained by an investment and a financing decision

Managing these decisions is a hard task, especially if you have to conduct the front-end of the business altogether

To this point, there has to be someone to organize these flows on behalf of the firm…

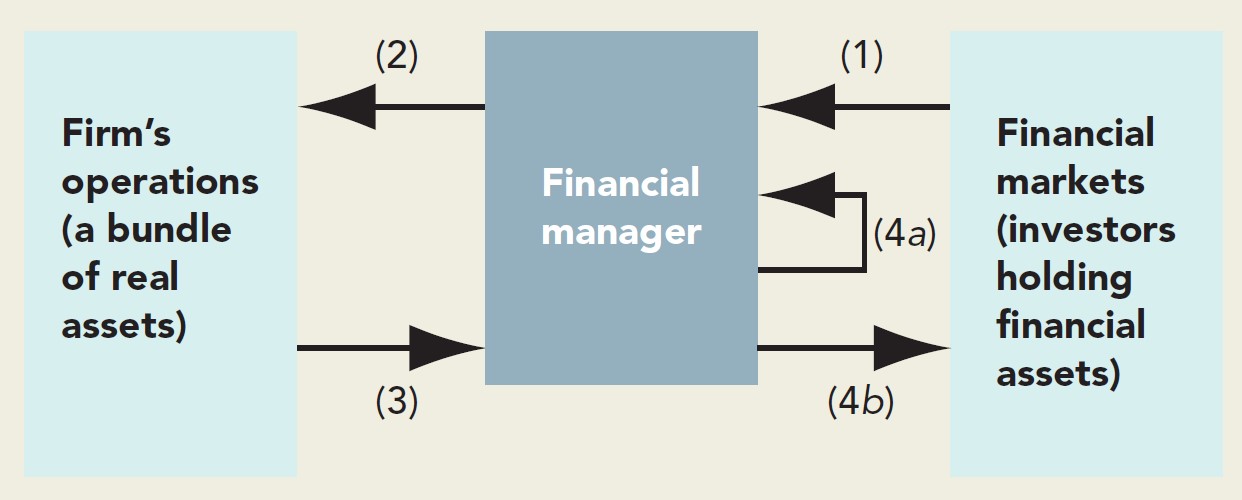

The role of the Financial Manager

- A Financial Manager1 stands between the firm and outside investors:

- On the one hand, it helps managing the firm’s operations, particularly by helping to make good investment decisions

- On the other hand, it deals with investors such as shareholders and financial institutions

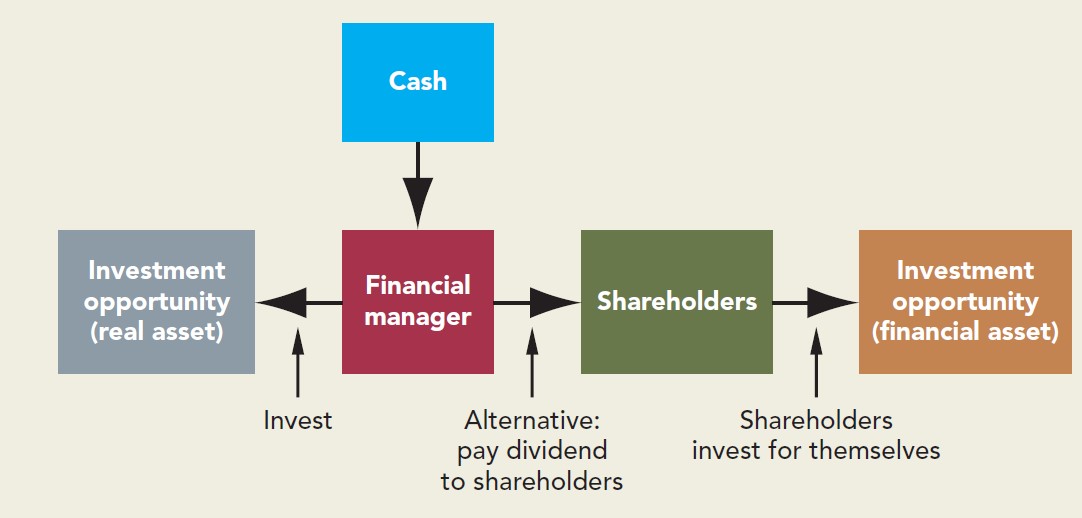

The Investment Trade-off

- Suppose that firm has a proposed investment project (a real asset) and has cash on hand to finance the project

- The Financial Manager has to decide whether to invest in the project:

- If investing, cash goes to fund the project

- If not investing, the firm can then pay out the cash to shareholders as an extra-dividend

References

![]()

Brealey, R. A., S. C. Myers, and F. Allen. 2020. Principles of Corporate Finance. The Irwin/McGraw-Hill Series in Finance, Insurance, and Real Estate. McGraw-Hill Education. https://books.google.com.br/books?id=nsrHuwEACAAJ.